Featured

Table of Contents

Overall insolvency filings rose 11 percent, with boosts in both company and non-business bankruptcies, in the twelve-month duration ending Dec. 31, 2025. According to stats launched by the Administrative Workplace of the U.S. Courts, annual insolvency filings totaled 574,314 in the year ending December 2025, compared with 517,308 cases in the previous year.

Non-business personal bankruptcy filings rose 11.2 percent to 549,577, compared with 494,201 in December 2024. Bankruptcy amounts to for the previous 12 months are reported four times annually.

For more on bankruptcy and its chapters, view the list below resources:.

As we enter 2026, the bankruptcy landscape is expected to move in methods that will substantially impact creditors this year. After years of post-pandemic unpredictability, filings are climbing up progressively, and economic pressures continue to affect consumer behavior.

Pros and Risks of Debt Settlement in 2026

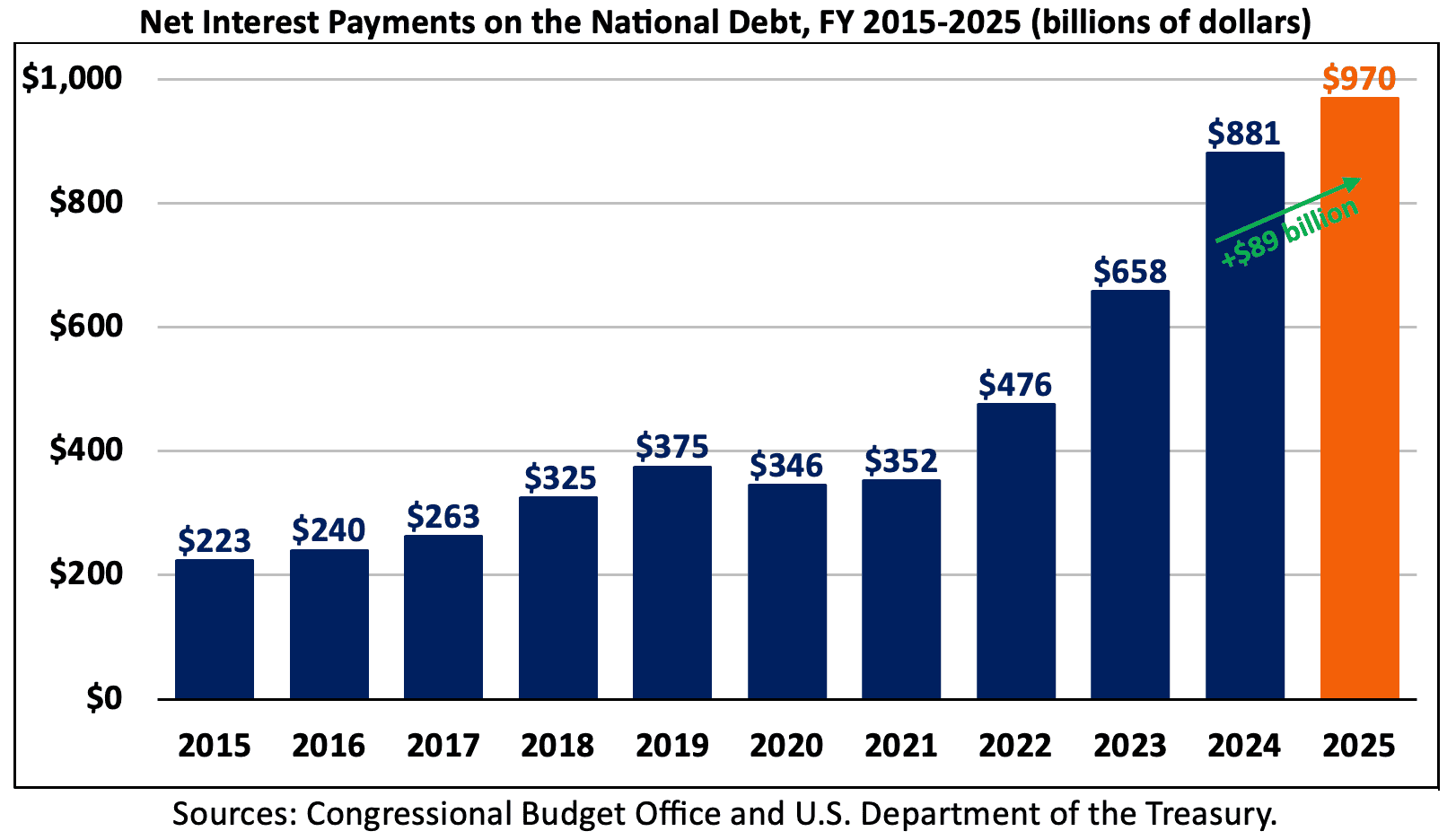

For a deeper dive into all the commentary and questions responded to, we advise viewing the full webinar. The most popular pattern for 2026 is a continual boost in insolvency filings. While filings have not reached pre-COVID levels, month-over-month growth recommends we're on track to exceed them quickly. Since September 30, 2025, bankruptcy filings increased by 10.6 percent compared to the previous fiscal year.

While chapter 13 filings continue to heighten, chapter 7 filings, the most typical type of customer insolvency, are anticipated to dominate court dockets., interest rates stay high, and borrowing expenses continue to climb.

Indicators such as customers utilizing "buy now, pay later on" for groceries and giving up just recently acquired vehicles demonstrate monetary stress. As a creditor, you may see more repossessions and vehicle surrenders in the coming months and year. You should also prepare for increased delinquency rates on car loans and mortgages. It's also essential to carefully keep an eye on credit portfolios as financial obligation levels remain high.

We forecast that the genuine effect will strike in 2027, when these foreclosures relocate to completion and trigger insolvency filings. Rising real estate tax and house owners' insurance coverage costs are already pushing novice delinquents into monetary distress. How can creditors remain one action ahead of mortgage-related insolvency filings? Your group must complete an extensive review of foreclosure processes, protocols and timelines.

Legitimate State Programs for Financial Relief

In current years, credit reporting in insolvency cases has ended up being one of the most contentious subjects. If a debtor does not declare a loan, you need to not continue reporting the account as active.

Resume normal reporting just after a reaffirmation agreement is signed and submitted. For Chapter 13 cases, follow the strategy terms carefully and seek advice from compliance groups on reporting responsibilities.

These cases typically develop procedural complications for financial institutions. Some debtors may stop working to properly reveal their properties, income and costs. Once again, these problems add intricacy to bankruptcy cases.

Some recent college grads may manage commitments and resort to bankruptcy to manage overall debt. The failure to perfect a lien within 30 days of loan origination can result in a creditor being dealt with as unsecured in insolvency.

:fill(white):max_bytes(150000):strip_icc()/PacificDebtRelief1-6af447bab4b44eb39929b3cf7d2cd871.jpg)

Our team's suggestions include: Audit lien excellence processes regularly. Maintain documents and proof of timely filing. Consider protective measures such as UCC filings when delays happen. The insolvency landscape in 2026 will continue to be shaped by economic unpredictability, regulative analysis and progressing customer habits. The more prepared you are, the easier it is to browse these difficulties.

Shielding Your Income From Creditor Harassment

By expecting the patterns pointed out above, you can reduce exposure and keep functional strength in the year ahead. If you have any concerns or issues about these forecasts or other personal bankruptcy topics, please link with our Personal Bankruptcy Healing Group or contact Milos or Garry directly any time. This blog site is not a solicitation for business, and it is not intended to make up legal recommendations on particular matters, produce an attorney-client relationship or be legally binding in any method.

With a quarter of this century behind us, we go into 2026 with hope and optimism for the brand-new year. However, there are a variety of concerns many sellers are grappling with, consisting of a high financial obligation load, how to use AI, diminish, inflationary pressures, tariffs and subsiding demand as affordability persists.

Reuters reports that high-end retailer Saks Global is preparing to apply for an impending Chapter 11 personal bankruptcy. According to Bloomberg, the business is going over a $1.25 billion debtor-in-possession financing package with creditors. The company regrettably is encumbered considerable financial obligation from its merger with Neiman Marcus in 2024. Included to this is the general global downturn in luxury sales, which might be crucial factors for a possible Chapter 11 filing.

Expert Guidance for Managing Financial InsolvencyThe business's $821 million in net revenue was down 4.5% year-over-year, driven by a 12% decline in hardware and a 27% decline in software sales. It is unclear whether these efforts by management and a better weather condition environment for 2026 will help prevent a restructuring.

According to a recent posting by Macroaxis, the odds of distress is over 50%. These problems combined with substantial debt on the balance sheet and more people skipping theatrical experiences to view films in the convenience of their homes makes the theatre icon poised for bankruptcy proceedings. Newsweek reports that America's most significant infant clothing retailer is planning to close 150 stores nationwide and layoff hundreds.

{kind=link}

Latest Posts

Ways to Protect Your Home During Insolvency

Regaining Financial Stability After Debt in 2026

Reliable Methods to Reduce Consumer Accounts