Featured

Table of Contents

American households are bring some of the greatest debt levels on record. With purchase APRs now averaging about 22%, numerous households discover that even paying the minimum each month barely damages their balances.

These business work out with lenders to minimize the total quantity owed on unsecured debts like credit cards or individual loans. While settlement can reduce balances, it's not without tradeoffs credit history can be affected, and taxes might apply on forgiven financial obligation. Not all companies in this area are equal. Some are recognized and have years of outcomes to indicate, while others run in less states or absence clear disclosures.

We limited this list to companies that specialize in financial obligation settlement programs where negotiators deal with financial institutions to decrease the overall amount you owe on unsecured debts. Business that just provide loans or credit therapy strategies were not included. The list below factors directed our rankings: Market accreditation: Validated membership with groups such as the American Association for Debt Resolution (AADR) or the Association for Consumer Financial Obligation Relief (ACDR). Cost structure: Programs that follow FTC rules and charge no in advance charges, with expenses collected only after a settlement is reached and a payment is made.

State schedule: How numerous states the business serves. Some operate almost across the country, while others are more minimal. Minimum debt requirement: The most affordable quantity of unsecured financial obligation required to enlist, frequently $7,500 or $10,000. Performance history and scale: Years in operation, number of accounts dealt with and recognition in independent rankings. Transparency and evaluations: Clear public disclosures, third-party ratings and customer feedback through the BBB or Trustpilot.

Established in 2009, it has become one of the biggest and most recognized financial obligation settlement business in the nation. The company is a certified member of the Association for Consumer Debt Relief, which signifies compliance with market standards.

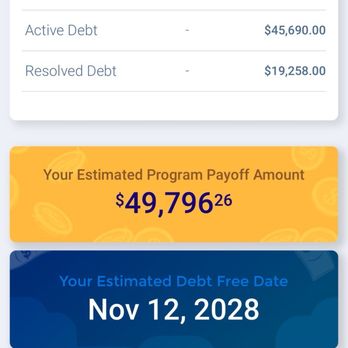

How Local Debt Partnerships Offer Relief

National Financial obligation Relief charges no upfront fees. Customers pay a fee normally in between 15% and 25% of the enrolled debt just after a settlement is reached and a payment is made. Programs are typically offered to people with a minimum of $7,500 in unsecured debt, and services encompass 46 states, more than some rivals.

Its debt settlement services focus on negotiating unsecured financial obligations such as credit cards and personal loans. Achieve normally requires a minimum of about $7,500 in unsecured financial obligation to enroll.

Charges generally fall within the industry variety of 15% to 25% and are only collected after a settlement is reached and a payment is made. Clients can evaluate and approve each settlement before it is completed. Achieve sticks out for its long operating history and structured customer tools. While financial obligation settlement is one part of a bigger product lineup, the business has actually earned solid customer reviews and preserves clear disclosures about costs and procedure.

For consumers who value a recognized business with incorporated financial tools and transparent settlement practices, Accomplish is a strong competitor. 2 Established in 2008, Americor is a financial obligation relief company that concentrates on debt settlement for unsecured debts such as credit cards and personal loans. The business belongs to the American Association for Debt Resolution, which reflects adherence to market standards.

Program charges normally fall within the market variety of 15% to 25% and are gathered just after a settlement is reached and a payment is made. Clients evaluate and authorize each settlement before it becomes last.

How Nonprofit Credit Counseling Helps

Availability is broad but not across the country, and services vary by state. Americor has received normally positive customer feedback, with solid rankings on platforms like the BBB and Trustpilot. 3 Developed in 2002 and headquartered in San Mateo, California, it is among the longest-running and largest debt settlement firms in the U.S.

Top Government Debt Relief Programs for 2026Freedom Financial obligation Relief programs typically need a minimum of $7,500 in unsecured financial obligation. Costs resemble rivals, usually ranging from 15% to 25%, and are only gathered after a settlement is reached and a payment is made. Clients have access to a consumer portal to track progress and can approve or decrease settlements before they are settled.

4 Accredited Debt Relief takes the fifth spot. Founded in 2011, it operates alongside Beyond Finance, LLC, which is listed as an accredited member of the ACDR.Accredited usually needs customers to have at least $10,000 in unsecured financial obligation to certify. Costs fall in the market series of 15% to 25%, gathered only after a debt is settled and a payment is made.

The business has earned positive marks in independent evaluations from Forbes Advisor and Bankrate. While its accessibility does not extend to all states, Accredited remains a popular name in the debt settlement market. 5 Financial obligation settlement can provide real relief for individuals struggling with high balances, but picking the best business matters.

Navigating the 2026 Insolvency Filing

Before registering, compare charges, schedule and reviews thoroughly to discover the very best suitable for your situation. Financial obligation settlement is a major monetary step, and dealing with a reputable company can make the procedure more transparent and efficient.

Home financial obligation in America is over 18 trillion dollars, according to the Federal Reserve Bank of St Louis. With so much debt, it's not surprising that many Americans desire to be debt-free.

Debt is constantly a financial burden. But it has actually become harder for many people to handle in recent years, thanks to increasing interest rates. Rates have increased in the post-COVID era in response to uncomfortable financial conditions, including a surge in inflation triggered by supply chain disruptions and COVID-19 stimulus spending.

While that benchmark rate doesn't straight control interest rates on financial obligation, it impacts them by raising or lowering the expense at which banks borrow from each other. Added expenses are usually handed down to clients in the kind of greater interest rates on debt. According to the Federal Reserve Board, for instance, the typical interest rate on charge card is 21.16% as of May 2025.

Card rates of interest might likewise increase or remain high into 2026 even if the Federal Reserve changes the benchmark rate, due to the fact that of growing creditor issues about increasing defaults. When financial institutions are scared clients will not pay, they often raise rates. Experian likewise reports average rates of interest on car loans struck 11.7% for used vehicles and 6.73% for brand-new automobiles in March 2025.

{kind=link}

Latest Posts

Ways to Protect Your Home During Insolvency

Regaining Financial Stability After Debt in 2026

Reliable Methods to Reduce Consumer Accounts